Summary

This proposal seeks community support to introduce a weETH/wstETH vault within the Fluid Protocol. The initiative aims to tap into the growing interest in the Liquid Restaking Token (LRT) space, particularly from protocols like ether.fi, to enhance the protocol’s competitiveness and market positioning. This proposal would introduce Wrapped Ether.Fi ETH (weETH) into the Fluid ecosystem.

Proposal

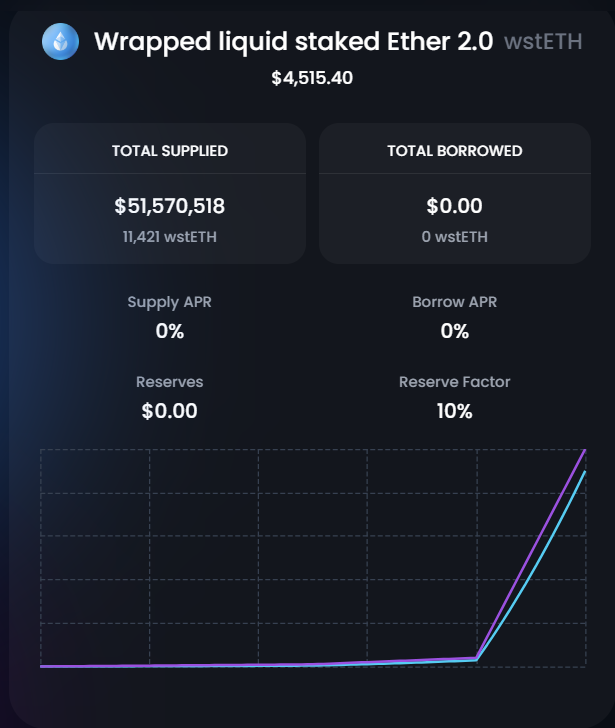

This proposal taps into the growing LRT market with the addition of a weETH/wstETH vault, capitalizing on the rapid expansion of the LRT segment and the unique position of Fluid to offer the market’s cheapest leverage. This move is anticipated to not only capture a significant share of the LRT market but will also bring utilization to the wstETH liquidity on Fluid that is currently not being utilized at all!

Recap of Fluid Vault Parameters

Fluid’s vault protocol features some familiar and as well as some new concepts for understanding the vault’s limits and parameters. See the following below:

C.F (Collateral Factor): Limit till which user can borrow.

L.T (Liquidation Threshold): Limit at which the user starts to get liquidated.

L.M.L (Liquidation Max Limit): Limit above which the user gets 100% liquidated.

L.P (Liquidation Penalty): Penalty at liquidations. Applied between L.T to L.M.L.

W.G (Withdrawal Gap): Extra gap on Liquidity Layer limits reserved for liquidations.

Liquidation Max Limit or L.M.L which denotes a level at which a position is fully liquidated. While most positions will incur liquidations over time the Liquidation Max Limit prevents the debt from becoming undercollateralized in a sudden downfall.

weETH/wstETH Vault Parameters:

The proposed vault will feature the following initial parameters:

- Collateral Factor (C.F.): 91%

- Liquidation Threshold (L.T.): 93%

- Max Liquidation Limit (L.M.L.): 95%

- Liquidation Penalty (L.P.): 1%

- Withdrawal Gap (W.G.): 5%

These parameters are set up to offer high LTVs which maintain a tight liquidation threshold. These limits may change over time as the vaults operate in a live environment. Liquidity, Dex routing and other factors may affect the vault. The team will monitor the overall health and liquidation rates and may propose adjustments to the vault parameters.

Summary of Changes to Fluid:

- List weETH/wstETH (Wrapped Ether.fi ETH/Wrapped Staked ETH) as a Vault

Reasons

Risks

The proposal acknowledges potential risks associated with the rapid growth of weETH and proposes monitoring weETH backing at the contract level to mitigate price manipulation and ensure robustness against major slashing events.weETH has experienced rapid growth over a short period of time driven by high incentives and speculation around the Eigen Layer. Such growth also comes with a risk of rapid unwinding if the new technology faces critical issues (EtherFi is 4x audited).

On-chain liquidity for weETH is sufficient to liquidate 8100 weETH at once with less than 1% slippage.

LRT Opportunity and Landscape

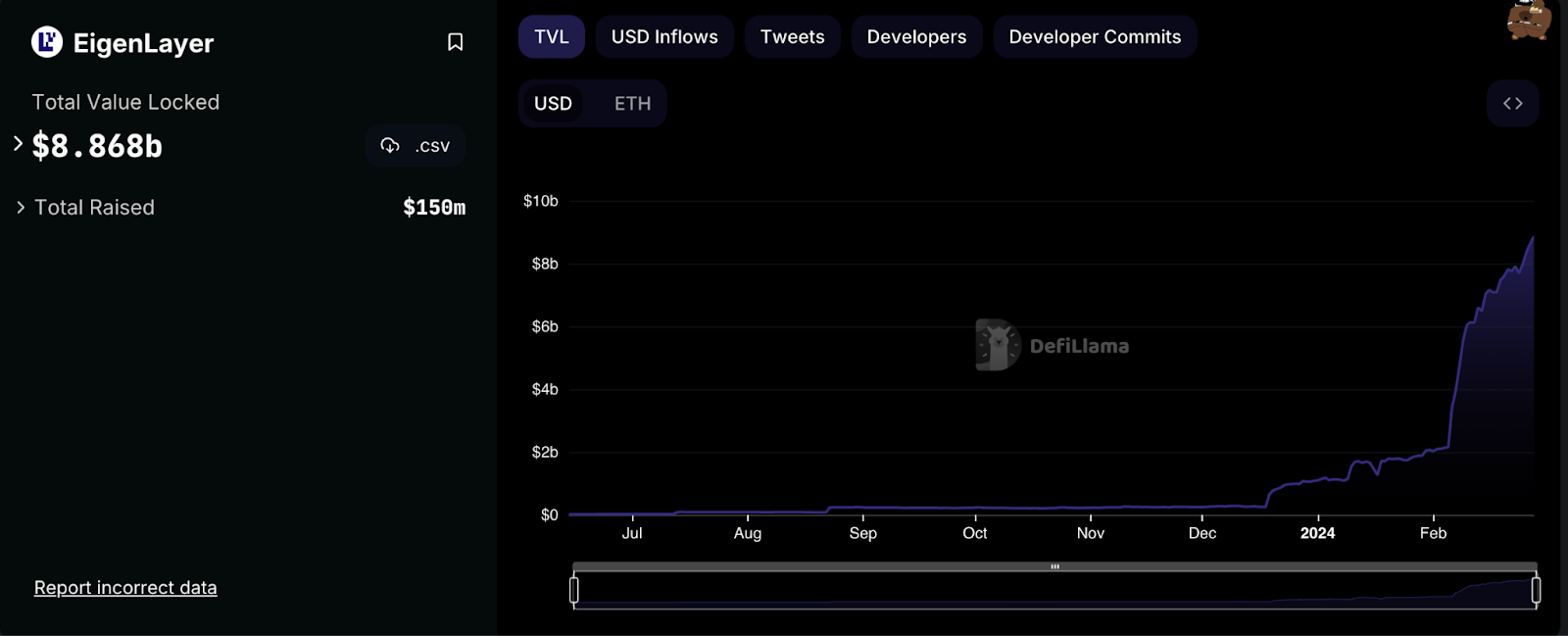

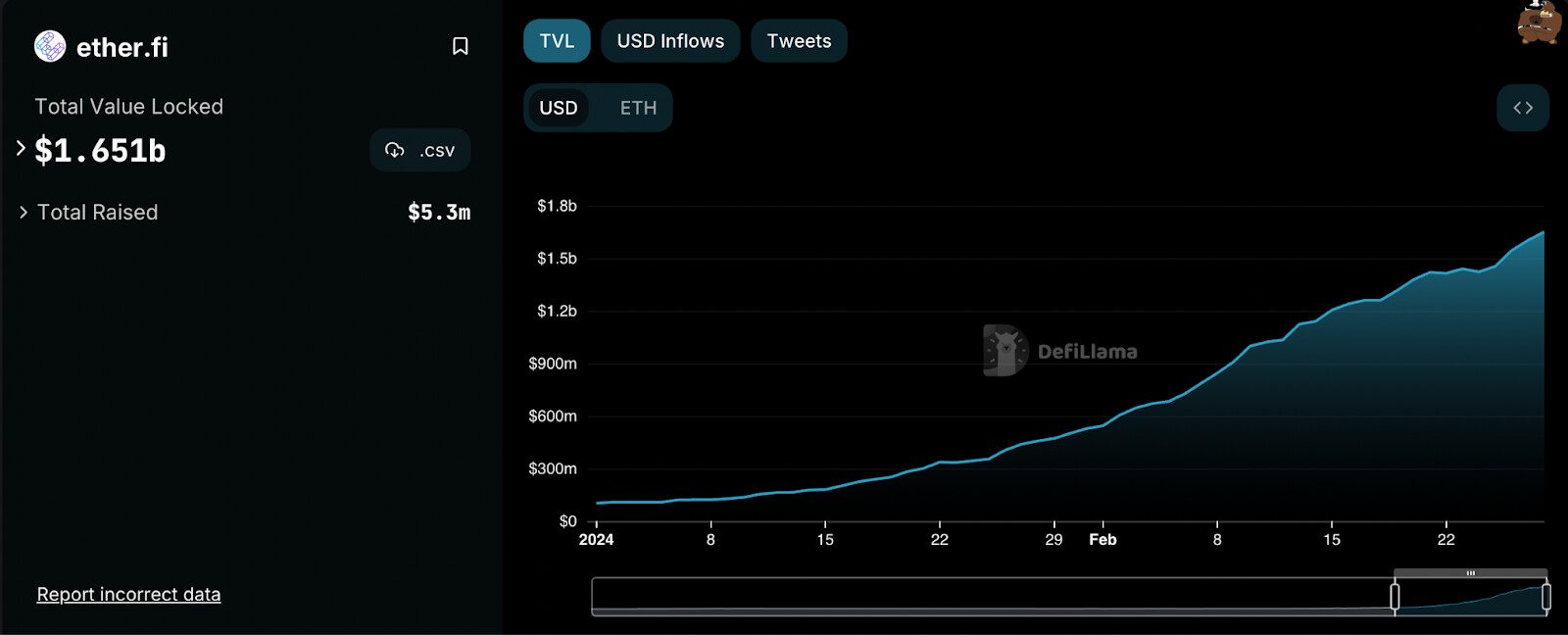

LRT space is one of the hottest and fastest-growing segments in DeFi right now. Eigen Layer, the biggest restaking protocol, has reached $8.9B TVL while EtherFi, the biggest staking protocol has reached $1.7B TVL in a matter of 2 months.

One of the reasons for their success is the Points system which allows users to farm future airdrops from multiple protocols at a time (EigenLayer + EtherFi). Other protocols that integrated LRTs have shown similar results.

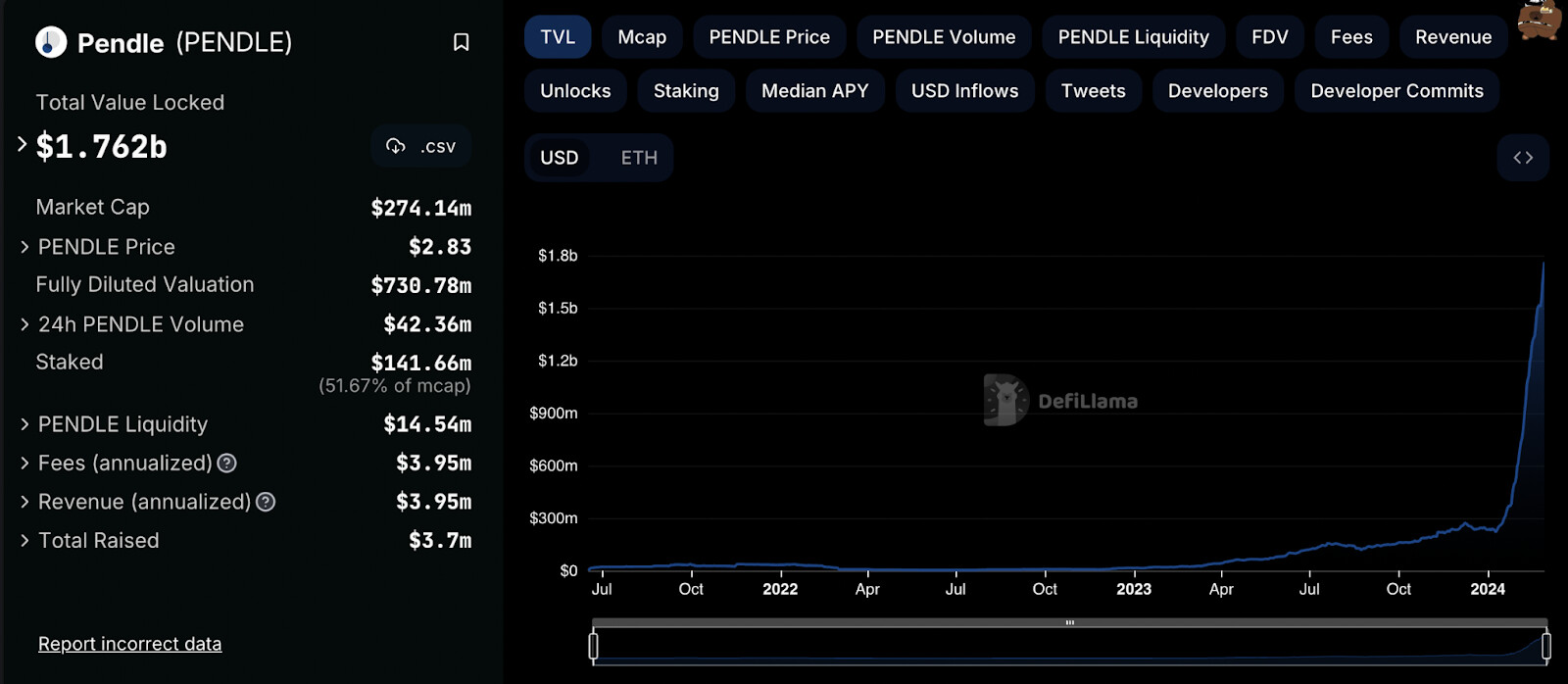

Pendle has grown from $200m to $1.8B TVL in 2 months:

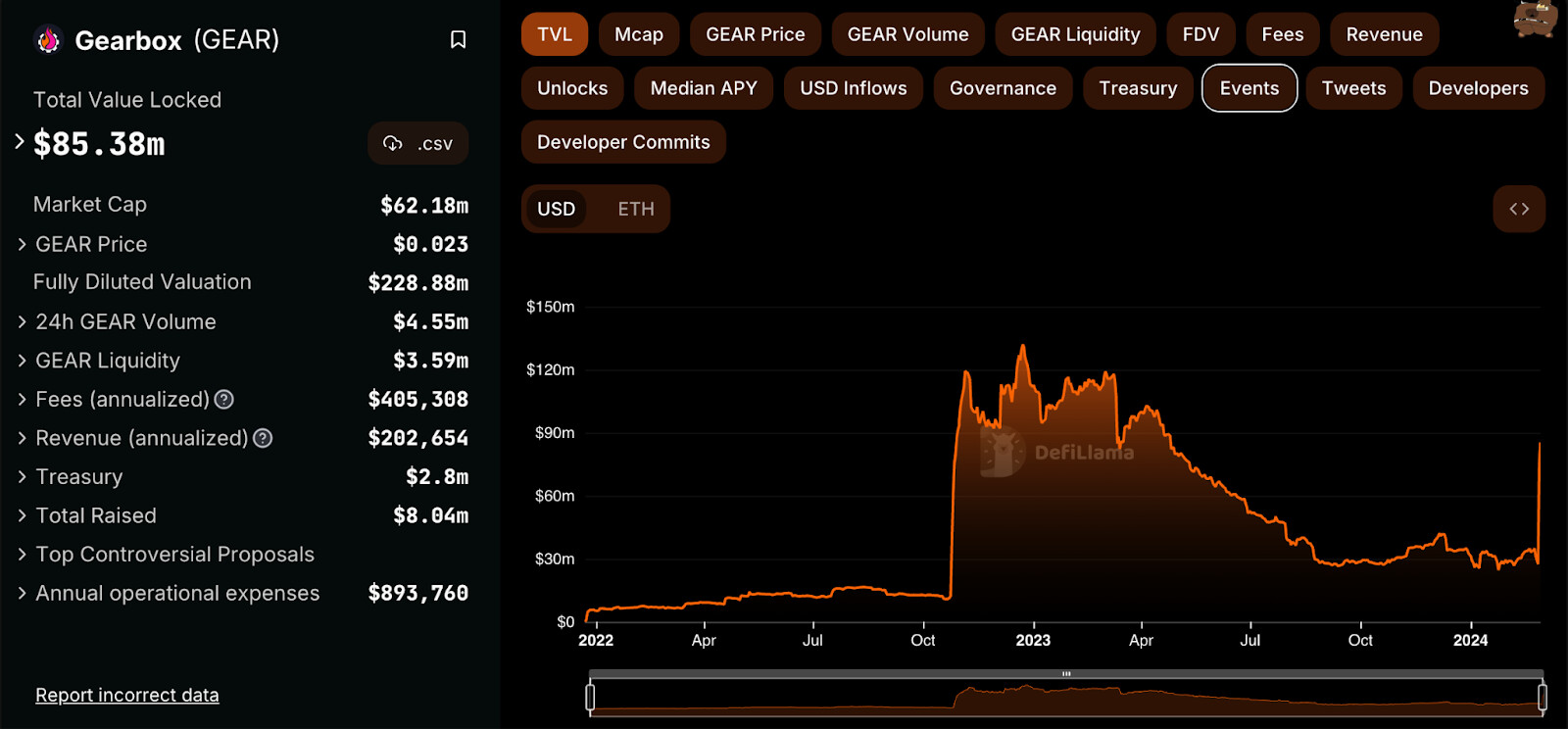

Gearbox recently integrated LRT and has shown incredible growth limited by the internal caps:

One of the main reasons for Pendle’s and Gearbox’s growth is the ability to leverage points by the users.

The cost of leverage on the above protocols is around 25%-30% APR.

By implementing weETH/ wstETH, Fluid would be able to offer the cheapest leverage on the market: weETH and wstETH native yield cancel each other and if Fluid applied the same interest rate model as on the ETH market, leverage cost would only be around 2-3% which is around 13 times cheaper than on other platforms (with the current Interest Rate Curve).

Moreover, with the recent proposal to add Fluid wstETH/ETH Vault to Lite Allocation Pools, adds to the utility of the wstETH liquidity in the Fluid protocol.

Fluid tapping into LRT space would potentially bring hundreds of millions in TVL increasing its revenue and adoption.

Result

The successful addition of the weETH/wstETH to the Vault protocol with the aforementioned parameters an on-chain vote is required from governance to finalize and approve this proposal.